Indian Ship Recycling Regains Momentum as Alang Climbs Regional Rankings Amid Currency Headwinds: STAR ASIA

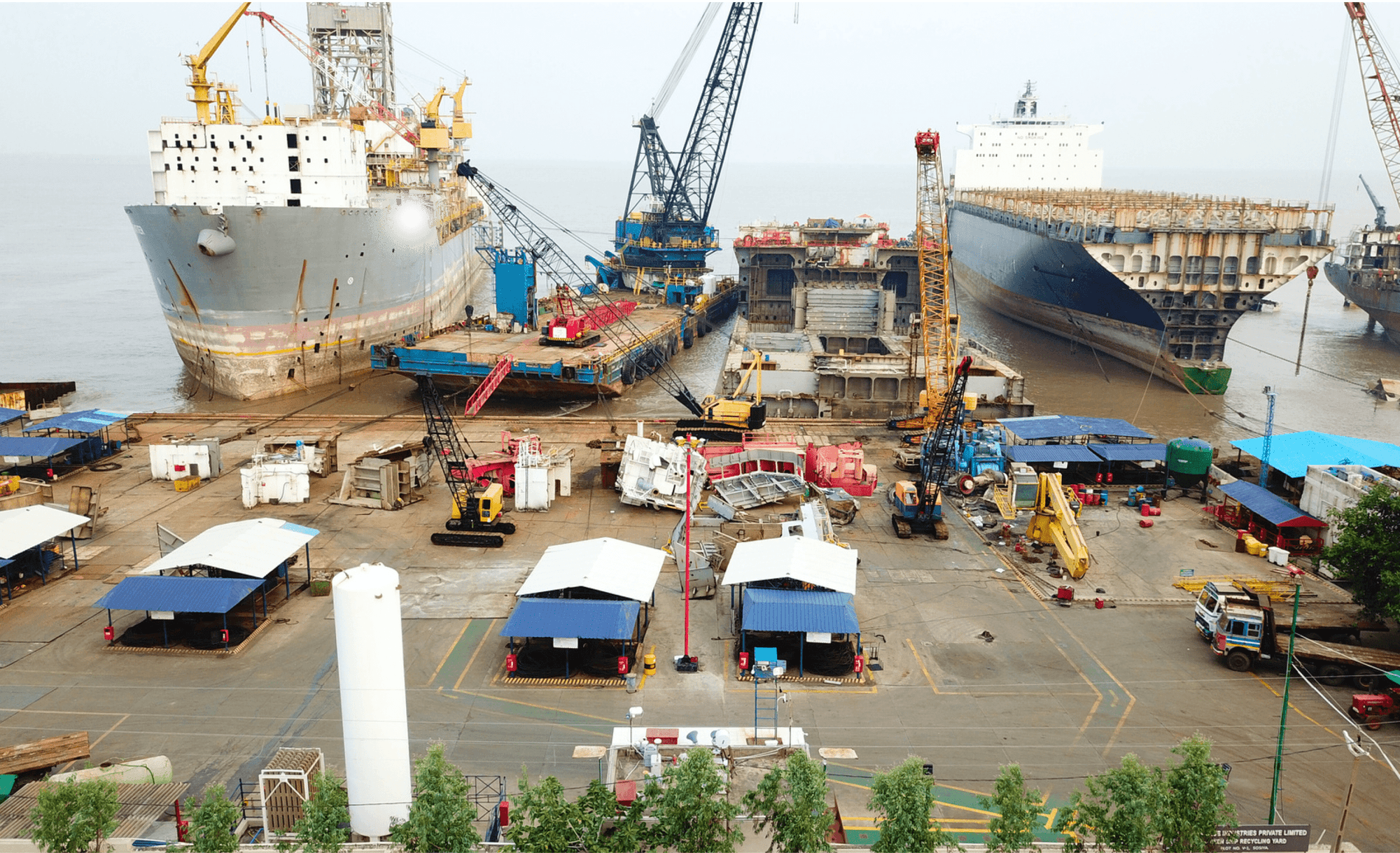

India’s ship recycling industry is showing renewed resilience, with Alang reclaiming the second position in regional price rankings, even as severe currency pressures and volatile commodity markets test the sector’s balance sheet. According to the latest weekly ship recycling market report by STAR ASIA Ship Brokers, Indian recyclers have managed to stay competitive despite the Indian Rupee sliding to around 91.65 against the US dollar, a level that has significantly increased import and financing costs.

The report underlines that Alang recyclers, operating under enormous financial stress, have nonetheless demonstrated tactical agility, outmanoeuvring more aggressive regional competitors to secure valuable tonnage, including another LNG carrier — a segment that remains highly sought-after due to its large light displacement tonnage (LDT) and relatively superior residual steel quality.

Alang: Competitive despite pressure

Alang’s resurgence comes at a time when domestic steel plate prices have been anything but stable. Prices dipped by nearly 2–4% earlier in the week, before recovering towards the end to hover around $410 per metric tonne. While such volatility typically dampens recycler sentiment, STAR ASIA notes that overall optimism in Alang remains intact, supported by a steady appetite for recycling opportunities and the persistent scarcity of available ships for demolition.

“Despite a continuing shortage of tonnage and fluctuations in steel prices, the mood in Alang is positive,” the report said, pointing to disciplined buying and cautious optimism among yard owners.

The anchorage and beaching data for January 2026 reflects moderate but steady activity. Vessels such as the tanker Global Star and reefer Yon Ang have already been beached, while several others, including tankers Woodchip and Yun Da You 6, and bulkers like Rising Harrier, remain at anchorage awaiting beaching clearance. Industry insiders say this pipeline, though not heavy, provides a degree of visibility for yards grappling with tight liquidity.

Chattogram: Recovery ahead of elections

Across the border in Bangladesh, Chattogram appears to be stabilising after a turbulent start to the year that saw it slip to the bottom of regional price tables. STAR ASIA reports that conditions have begun to improve, with buyers cautiously re-entering the market ahead of the country’s key February elections.

While demand for smaller and marginal units remains subdued, there is growing interest in high-value assets. This selective bidding behaviour reflects both risk aversion and constrained liquidity, as recyclers await political clarity. Steel plate prices in Bangladesh have remained stable at around $500 per tonne, offering recyclers some margin comfort, while the Bangladeshi Taka has held relatively steady near 122.26 against the dollar.

Recent arrivals, including tankers Fuji and Hakata and bulker Hong Li, are currently at anchorage, while larger units like the tanker Vigo have already been beached. Market participants believe that if elections pass smoothly and liquidity improves, Bangladesh could quickly regain its traditional leadership position in the subcontinent’s ship recycling market.

“A stable government is key,” the report noted. “Once political uncertainty fades, Bangladesh is expected to free up funding lines, allowing recyclers to bid more aggressively.”

Gadani: Confidence without activity

Pakistan’s Gadani yards present a contrasting picture. Domestic sentiment has improved, driven largely by a decline in the inflow of low-cost Iranian steel products. This has created an opportunity for local steel mills, which are now increasingly looking towards ship recyclers for raw material supply.

Despite this improved outlook and Gadani sitting at the top of the regional price board, physical activity at the waterfront remains conspicuously muted. STAR ASIA observes that while end buyers have raised their bid levels, actual beachings have yet to materialise, as Gadani recyclers face stiff competition from Indian and Bangladeshi buyers for the limited number of available ships.

For January 2026, no vessels were reported at anchorage or beaching at Gadani, underscoring the disconnect between pricing optimism and on-ground activity.

Turkey and global bunker trends

Outside the subcontinent, the Aliaga ship recycling market in Turkey remains unchanged, with no new activity reported during the week. Outlook for the region remains steady, with buyers adopting a wait-and-watch approach as they head into the new month.

Meanwhile, global bunker prices showed mixed trends across major ports. Singapore’s VLSFO stood at $465 per tonne, while Rotterdam offered lower levels at $433. Marine gasoil (MGO) remained elevated across regions, reflecting ongoing tightness in refined fuel markets.

Currency movements also played a critical role in shaping recycler sentiment. While the Indian Rupee weakened marginally week-on-week, the Bangladeshi Taka and Pakistani Rupee remained largely stable. The Turkish Lira showed slight appreciation, though inflationary pressures continue to weigh on local costs.

Scrap markets: Defensive strategies dominate

Beyond ship recycling, ferrous scrap markets across the subcontinent and Turkey continue to influence demolition pricing and sentiment.

In India, the imported scrap market remains subdued, as the depreciating rupee and stagnant finished steel demand push buyers into a defensive posture. A clear north-south price disparity has emerged, with North India trading about $10–$15 per tonne higher than the south. HMS 80:20 is currently assessed near $350 CFR Mundra in the north, compared to around $335 CFR Chennai in the south. Australian-origin scrap offers into Chennai, including HMS at $330 and shredded scrap at $350, have faced resistance amid soft southern demand.

Pakistan, by contrast, has seen relatively more active supplier interest. Imported shredded scrap from the UK and EU is being offered around $380 CFR, with UAE suppliers seeking $395 or higher. HMS grades are trading between $365 and $375 CFR, keeping Pakistan attractive for overseas sellers. Domestic scrap prices remain elevated at PKR 135,000–136,000 per tonne, equivalent to roughly $483–$486.

Bangladesh’s imported scrap market has remained stable but cautious. Japanese H2 scrap is quoted around $355–$357 CFR Chattogram, while HMS 80:20 trades at $345–$350. Premium plate and structural scrap continues to command $370–$375 CFR, indicating steady demand but disciplined purchasing.

Turkey’s scrap market, meanwhile, witnessed what STAR ASIA described as a “silent week.” Deep-sea import prices have reached a friction point, with European sellers facing breakeven levels in the high $370s CFR. Turkish mills, constrained by weak rebar sales, have largely stayed away from fresh bookings, resulting in a stalemate.

Outlook: Cautious optimism

The broader outlook for global ship recycling remains cautiously optimistic, though heavily dependent on currency movements, political developments, and steel demand. For India, Alang’s ability to regain regional standing despite a sharply weaker rupee underscores the industry’s adaptability and long-term relevance in global ship disposal.

As shipping markets continue to grapple with overcapacity and ageing fleets, recyclers across the subcontinent are positioning themselves for a potential uptick in demolition activity later in the year. For now, disciplined buying, selective risk-taking, and close attention to macroeconomic signals remain the defining features of the market.

For Indian recyclers, the message is clear: while financial headwinds persist, strategic positioning and operational efficiency are keeping Alang firmly in the global ship recycling conversation.

Author: shipping inbox

shipping and maritime related web portal